Wednesday, December 30, 2009

Monday, December 28, 2009

The Economy 2010 and Beyond

Is it a bounce or a bull market? We’ll stick with the bounce hypothesis a while longer; until we’re proven right…or people start laughing at us, whichever comes first.

Meanwhile, the man on the street is not taking chances. While he probably believes the claptrap from Washington and Wall Street, he also knows that his house has lost 30% of its value and that if he loses his job he’ll have a hard time finding another one. So, he’s cutting back – just like he should...

The economy can’t go back to the Bubble Epoque. That period was irreproducible. Consumers were able to live beyond their means by borrowing against their houses (or, ‘taking out equity,’ as they liked to say.) Those days are gone forever...

Depressions take time to express themselves. Remember, they are not pauses in the life of an otherwise healthy trend. They are what happens after the trend drops dead. Then, the economy needs to reinvent itself. At first, people don’t want to believe it. They try to revive the old business model. They bet that the old companies will quickly return to robust health; they buy their stocks. They demand that the government do something to save the poor, ailing economy.

But it’s not that simple… You can’t revive a dead economy. And when you realize the old economic model is, in fact, a corpse…it’s depressing.

The US economy (and much of the rest of the world economy) can no longer depend on increasing consumer debt. We need a new model…a new business plan… The sooner we find one, the better off we all will be.

read the entire essay

Meanwhile, the man on the street is not taking chances. While he probably believes the claptrap from Washington and Wall Street, he also knows that his house has lost 30% of its value and that if he loses his job he’ll have a hard time finding another one. So, he’s cutting back – just like he should...

The economy can’t go back to the Bubble Epoque. That period was irreproducible. Consumers were able to live beyond their means by borrowing against their houses (or, ‘taking out equity,’ as they liked to say.) Those days are gone forever...

Depressions take time to express themselves. Remember, they are not pauses in the life of an otherwise healthy trend. They are what happens after the trend drops dead. Then, the economy needs to reinvent itself. At first, people don’t want to believe it. They try to revive the old business model. They bet that the old companies will quickly return to robust health; they buy their stocks. They demand that the government do something to save the poor, ailing economy.

But it’s not that simple… You can’t revive a dead economy. And when you realize the old economic model is, in fact, a corpse…it’s depressing.

The US economy (and much of the rest of the world economy) can no longer depend on increasing consumer debt. We need a new model…a new business plan… The sooner we find one, the better off we all will be.

read the entire essay

Bush: Big Spender

Figure 1 shows the average increase in total spending under recent presidents. Bush II was the biggest spender since LBJ. His spending increases were far larger than the three prior presidents.

Of course, presidents share spending power with Congress and it is easier for presidents to control discretionary spending than entitlement spending. Nonetheless, the results in these charts reflect the general spending approach taken by the presidents quite well. For example, Bush II was instrumental in adding the Medicare drug benefit, which by 2009 was adding more than $60 billion a year to federal spending.

US Manufacturing

If the U.S. manufacturing sector were a separate country, it would be tied with Germany as the world's third largest economy. It would also be larger than the entire economies of India and Russia combined. As much as we hear about the "demise of U.S. manufacturing," and how we are a country that "doesn't produce anything anymore," and how we have "outsourced our production to China," the U.S. manufacturing sector is alive and well, and the U.S. is still the largest manufacturer in the world.

If the U.S. manufacturing sector were a separate country, it would be tied with Germany as the world's third largest economy. It would also be larger than the entire economies of India and Russia combined. As much as we hear about the "demise of U.S. manufacturing," and how we are a country that "doesn't produce anything anymore," and how we have "outsourced our production to China," the U.S. manufacturing sector is alive and well, and the U.S. is still the largest manufacturer in the world.

Workers today produce twice as much manufacturing output as their counterparts did in the early 1990s, and three times as much as in the early 1980s, thanks to innovation and advances in technology that have made today’s workers the most productive in history.

Financial Meltdown Article

Lost Trust: The Real Cause of the Financial Meltdown

by Bruce Yandle

Accounting standards, credit ratings, and credit-default swaps were created to help facilitate financial transactions by fostering trust. In the run-up to the credit-market freeze of 2008 those assurance mechanisms collapsed under the weight of political and regulatory pressures to aggressively expand homeownership and other policies.

read the article

by Bruce Yandle

Accounting standards, credit ratings, and credit-default swaps were created to help facilitate financial transactions by fostering trust. In the run-up to the credit-market freeze of 2008 those assurance mechanisms collapsed under the weight of political and regulatory pressures to aggressively expand homeownership and other policies.

read the article

Sunday, December 27, 2009

The Problem is Central Banking

PRESIDENT BARACK OBAMA HEADS the list of Americans who believe that the continuing financial crisis should be blamed on excessive risk-taking by bankers who had an unbridled desire to make money in mortgages. These would-be reformers want stronger government regulation of the bankers to make sure that nothing like this ever happens again...

A deeper examination, however, reveals that this is neither a housing crisis nor a Wall Street banking crisis. This is a monetary crisis, rooted in the lending of money created out of thin air. This is what leads to economic booms and busts.

The current crisis goes back to the Asian Contagion of 1997 and the meltdown of the Long Term Capital Management hedge fund in 1998. In response to each of these situations, the Federal Reserve cut interest rates and rapidly expanded the money supply...

Healthy economic growth is supported by savings, rather than newly created money. People and businesses save and invest the money they don't need to consume right away. They make loans and investments that create computer equipment, copper mines, retail stores, and new homes...

How many more crises must we endure until we realize the common denominator is the creation of money and credit by the Fed? Wall Street bankers and speculators, who try to game the system and make profits during each boom, are mere bit players in these crises. By fostering the booms and triggering the busts, the real villain is the institution of central banking itself. Thus, instead of providing stability to the economy, central banking has created great instability. Until this is understood, we will make little progress in preventing future crises or easing the current one.

Lurching from crisis to crisis in boom-bust fashion is unacceptable and unnecessary. The Federal Reserve must stop juicing the economy with massive amounts of newly created money and move to a monetary system free of government-caused booms and busts.

source

A deeper examination, however, reveals that this is neither a housing crisis nor a Wall Street banking crisis. This is a monetary crisis, rooted in the lending of money created out of thin air. This is what leads to economic booms and busts.

The current crisis goes back to the Asian Contagion of 1997 and the meltdown of the Long Term Capital Management hedge fund in 1998. In response to each of these situations, the Federal Reserve cut interest rates and rapidly expanded the money supply...

Healthy economic growth is supported by savings, rather than newly created money. People and businesses save and invest the money they don't need to consume right away. They make loans and investments that create computer equipment, copper mines, retail stores, and new homes...

How many more crises must we endure until we realize the common denominator is the creation of money and credit by the Fed? Wall Street bankers and speculators, who try to game the system and make profits during each boom, are mere bit players in these crises. By fostering the booms and triggering the busts, the real villain is the institution of central banking itself. Thus, instead of providing stability to the economy, central banking has created great instability. Until this is understood, we will make little progress in preventing future crises or easing the current one.

Lurching from crisis to crisis in boom-bust fashion is unacceptable and unnecessary. The Federal Reserve must stop juicing the economy with massive amounts of newly created money and move to a monetary system free of government-caused booms and busts.

source

Gold: The Trade of the Decade

“A $100 investment in gold would now be more than $380,” Bloomberg calculates, “while the same sum in commodities would have grown to about $357, according to the Standard & Poor’s GSCI Enhanced Total Return Index.”

“A $100 investment in gold would now be more than $380,” Bloomberg calculates, “while the same sum in commodities would have grown to about $357, according to the Standard & Poor’s GSCI Enhanced Total Return Index.”source

The Debt Bubble

We also highlighted some of the disturbing New Math that this chart implied. Specifically, we reported, “The government will have to cough up $1.6 trillion just by the end of March. Ten years from now, the mere cost of servicing the debt is expected to reach $700 billion annually, more than three times the current burden.”...

Saturday, December 26, 2009

Tuesday, December 22, 2009

2009 3rd Quarter GDP Declines to 2.2%

Estimates of the growth rate for the U.S. economy are starting to sound more and more like earnings estimates - you hear everyone talking about much larger numbers for months and months and then, when the final figures are reported, they prove to be a bit disappointing, in this case revised down from 3.5 percent, to 2.8 percent, to a final reading of 2.2 percent.

Friday, December 18, 2009

Central Banking and Central Planning

What is being ignored is the more fundamental question of whether the Fed should be attempting to set or influence interest rates in the market. The presumption is that it is both legitimate and desirable for central banks to manipulate a market price, in this case the price of borrowing and lending. The only disagreements among the analysts and commentators are over whether the central banks should keep interest rates low or nudge them up and if so by how much...

At the heart of the problem is that fact that the Federal Reserve’s manipulation of the money supply prevents interest rates from telling the truth: How much are people really choosing to save out of income, and therefore how much of the society’s resources – land, labor, capital – are really available to support sustainable investment activities in the longer run? What is the real cost of borrowing, independent of Fed distortions of interest rates, so businessmen could make realistic and fair estimates about which investment projects might be truly profitable, without the unnecessary risk of being drawn into unsustainable bubble ventures?

Unfortunately, as long as there are central banks, we will be the victims of the monetary central planners who have the monopoly power to control the amount of money and credit in the economy; manipulate interest rates by expanding or contracting bank reserves used for lending purposes; threaten the rollercoaster of business cycle booms and busts; and undermine the soundness of the monetary system through debasement of the currency and price inflation.

Interest rates, like market prices in general, cannot tell the truth about real supply and demand conditions when governments and their central banks prevent them from doing their job. All that government produces from their interventions, regulations and manipulations is false signals and bad information. And all of us suffer from this abridgement of our right to freedom of speech to talk honestly to each other through the competitive communication of market prices and interest rates, without governments and central banks getting in the way.

read the entire essay

My thoughts: An outstanding essay explaining why the Fed is doing more harm than good.

Thursday, December 17, 2009

source

source

Wednesday, December 16, 2009

Peter Schiff on the Economy

Although Barack Obama has refrained, at least for now, from delivering triumphant speeches in a naval flight suit, there is nevertheless a strong tone of accomplishment emanating from the President and his deputies. Over the weekend, top White House economic adviser Lawrence Summers even pronounced that the recession is now over. Without hedging his bets, Summers declared that thanks to the Obama Administration's wise stewardship, economic stimuli, and emergency bailouts, another Great Depression, set up by the prior Administration, had been narrowly averted. Summers saw no impediments to the return of sustainable growth. He may as well have delivered these remarks from the deck of an aircraft carrier.

I hate to shoot down these high-flying expectations, but the economy is not improving. All that has changed is that we are now more indebted to foreign creditors, with even less to show for it. Washington's current policies have once again deferred the fundamental, market-driven reforms needed to redirect us onto a sustainable path. Instead, through aggressive monetary and fiscal stimuli, we are trying to re-inflate a balloon that is full of holes. This was the Bush Administration's exact response to the 2002 recession. It's shocking how few observers note the repeating pattern, especially the fact that each crash is worse than the last...

First, a closer look at the jobs numbers shows that employment improved in sectors that benefited most directly from monetary or fiscal stimulus: government, healthcare, financial services, education and retail sales...

Second, major investment and commercial banks are not back on their feet, but remain fundamentally insolvent...

Third, while it is true that home prices have stopped falling, this represents failure, not victory...

Finally, it is true that the GDP yardstick shows an economy returning to growth. However, as I have often repeated, this measure has deep flaws that render it almost useless for judging the soundness of an economy...

But for now, the chattering classes believe strong government action has delivered us from calamity. For them, at least, it's “mission accomplished!”

Tuesday, December 15, 2009

Monday, December 14, 2009

Paul Samuelson Dies

Mr. Samuelson, the first American to win the Nobel Prize in economics and the author of a ubiquitous college textbook, was "one of the greatest teachers that economics has ever known" and "a titan of economics," said Federal Reserve Chairman Ben Bernanke, a former student of Mr. Samuelson's at the Massachusetts Institute of Technology...

In 1970, Mr. Samuelson was the first American to win the Nobel Prize in economics, the second year the prize was offered. "Samuelson's contribution has been that, more than any other contemporary economist, he has contributed to raising the general analytical and methodological level in economic science," wrote the Nobel prize committee. "He has in fact simply rewritten considerable parts of economic theory."

from the Wall Street Journal

Samuelson was fully aware of his world-wide influence. He declared that "I don't care who writes a nation's laws -- or crafts its advanced treatises -- if I can write its economics textbooks".

In his textbook he praised central planning and predicted the future higher standard of living in the communist world...

Unfortunately for all of us, almost everything that this truly gifted and talented man said, wrote and believed in resulted in less freedom, bigger government and widespread poverty here and around the world.

Requiem for Samuelson

An evil man who should be remembered along with Stalin and Hitler. May he be rotting in Hell now.

S.M. Olivia

In 1970, Mr. Samuelson was the first American to win the Nobel Prize in economics, the second year the prize was offered. "Samuelson's contribution has been that, more than any other contemporary economist, he has contributed to raising the general analytical and methodological level in economic science," wrote the Nobel prize committee. "He has in fact simply rewritten considerable parts of economic theory."

from the Wall Street Journal

Samuelson was fully aware of his world-wide influence. He declared that "I don't care who writes a nation's laws -- or crafts its advanced treatises -- if I can write its economics textbooks".

In his textbook he praised central planning and predicted the future higher standard of living in the communist world...

Unfortunately for all of us, almost everything that this truly gifted and talented man said, wrote and believed in resulted in less freedom, bigger government and widespread poverty here and around the world.

Requiem for Samuelson

An evil man who should be remembered along with Stalin and Hitler. May he be rotting in Hell now.

S.M. Olivia

Friday, December 11, 2009

Obama's Economic Policy: A Critique

As the government runs from one whimsical plan to another, all that market participants can be sure of is that there will be more regulation and intervention, and that the people will be soaked by taxes either direct or indirect. Since businesses are unsure of the economic environment, but rightfully anticipating (though, in my opinion, underestimating) an increase in outright socialism, this uncertainty will surely quell economic growth.

Thus, we see that Obama's policies are not only misguided but also incredibly destructive. If instead of letting the economy liquidate, painful as it may be, we try to continue the illusory boom, we will be doomed to years of unemployment, stagnation, and ultimately the "crack-up boom" of the economy. And this isn't even to mention the threats posed to our economy by national healthcare, cap-and-tax, and, even scarier, Mr. Obama's foreign policy.

Each and every one of these policies retards the necessary adjustment, depriving businesses of valuable assets that can be put to more profitable lines of work and depriving consumers of the products they seek at true fair-market value. The only way to create jobs and fix a broken economic model is to release the entrepreneurial forces of America. Unfortunately, it appears that President Obama does not care for this solution, preferring to ensure a prolonged depression to serve his political ends.

read the entire essay

Thus, we see that Obama's policies are not only misguided but also incredibly destructive. If instead of letting the economy liquidate, painful as it may be, we try to continue the illusory boom, we will be doomed to years of unemployment, stagnation, and ultimately the "crack-up boom" of the economy. And this isn't even to mention the threats posed to our economy by national healthcare, cap-and-tax, and, even scarier, Mr. Obama's foreign policy.

Each and every one of these policies retards the necessary adjustment, depriving businesses of valuable assets that can be put to more profitable lines of work and depriving consumers of the products they seek at true fair-market value. The only way to create jobs and fix a broken economic model is to release the entrepreneurial forces of America. Unfortunately, it appears that President Obama does not care for this solution, preferring to ensure a prolonged depression to serve his political ends.

read the entire essay

Thursday, December 10, 2009

Wednesday, December 9, 2009

The Fed: Academics v. Populist

A group of academic economists — including several Nobel Prize winners, leaders of respected economic journals and former Fed officials — is dialing up its call for lawmakers to drop plans to subject the Federal Reserve to more scrutiny by the Government Accountability Office, an investigative arm of Congress.

In a letter to leaders on the Senate Banking Committee and House Financial Services Committee, the economists say a bill proposed by Rep. Ron Paul (R., Tex.) and Alan Grayson (D., Fla.) to let the GAO review Fed monetary policy would do “serious harm to the economy.” They warn increased congressional oversight would harm the Fed’s independence and ability to fight inflation.

Mr. Paul has built a popular movement in part on his attacks against the Fed and won large support in the House for his bill. Ben Bernanke, Fed chairman, has a growing body of academics on his side. Some 270 economists have signed the letter, including Edward Prescott, Myron Scholes, Daniel McFadden, Fynn Kydland, Roger Myerson and Robert Engel, all Nobel winners.

source

My thoughts: The Fed has two major goals: promote economic growth and price stability.

They have failed on both counts. The first failure is obvious as we are mired in one of the deepest and longest post WWII recessions. The second should be obvious, but unfortunately it is not. The dollar has lost roughly 95% of its value since the creation of the Fed. This is not price stability. We have been conditioned to think in nominal terms. Too many people believe that 2-3% annual is normal or desirble; it is neither. Auditing the Fed is the first step toward ultimately killing the creature from Jekyll Island.

Tuesday, December 8, 2009

Falling Dollar: Winners and Losers

Since 2002, the dollar has lost about a third of its value compared with other currencies. That doesn't sound good — and it's not, if you're a Japanese exporter or an American tourist. But it is potentially great news for American workers.

Experts argue about the many effects of the dollar's fall and what it says about confidence in the American economy, with its decades-old trade deficit and mounting national debt. But there are also more predictable effects replayed in each decline.

Last week, as President Obama convened a summit meeting on unemployment, the devalued dollar was already doing its part to create jobs by making American goods cheaper abroad.

"I don't think anything they can come up with is as powerful as the dollar declining," said Kenneth S. Rogoff, a Harvard economist. "It's a good short-term boost. Every country's manufacturing sector loves it when the currency has a moderate depreciation."

But the benefit to American exporters goes only so far. Some economists say it hurts industry in the long run: companies can reap the rewards of the falling dollar without improving products or productivity. When the dollar rebounds, they falter anew.

Monday, December 7, 2009

Book Review: Where Keynes Went Wrong

Where Keynes Went Wrong by Hunter Lewis

reviewed by David Gordon

Defenders of Keynes, such as the recent convert Bruce Bartlett, often claim that he supported capitalism. (Bartlett's The New American Economy has this as a primary theme.) His interventionist measures had as their aim not the replacement of capitalism by socialism or fascism. Rather, it is alleged, Keynes aimed to save the existing order.

The unhampered market cannot by itself recover from a severe depression or at best can do so after long years of privation and unemployment. Keynes discovered a way by which the government, through an increase in spending, can restore the economy to prosperity. Only diehard purists could spurn Keynes's gift to capitalism. Without it, would not revolutionary pressure mount in a severe depression to overturn capitalism and replace it with socialism or fascism?

Hunter Lewis convincingly shows the error of this often-heard line of thought. Keynes, far from being the savior of capitalism, aimed to replace free enterprise with a state-controlled economy run by "experts" like him. His prescriptions for recovery from depression do not save capitalism: they derail the price system by which it functions. As one would expect, Keynes lacks sound arguments to support his revolutionary proposals. Quite the contrary, Keynes defied common sense and willfully resorted to paradox.

Indeed, as Lewis points out, the entire Keynesian edifice rests on a central paradox: impeding the central mechanism of the free market will restore prosperity. The free market works by price adjustments. If, e.g., consumers demand more of a product than is currently available, suppliers will raise their prices so that no imbalance exists. As consumers shift their demand from product to product, businesses must adjust their production schedules to meet changing preferences. If firms fail to do so, they face extinction...

Lewis's book is an ideal guide to Keynes's dangerous and destructive economics.

Sunday, December 6, 2009

Ben Bernanke Under Fire

Jim Bunning on Ben Bernanke:

Alan Greenspan refused to look for bubbles or try to do anything other than create them...

Under your watch, the Bernanke Put became a bailout for all large financial institutions...

But since then, you have decided that just about every large bank, investment bank, insurance company, and even some industrial companies are too big to fail. Rather than making management, shareholders, and debt holders feel the consequences of their risk-taking, you bailed them out. In short, you are the definition of moral hazard...

Even if all that were not true, the A.I.G. bailout alone is reason enough to send you back to Princeton...

From monetary policy to regulation, consumer protection, transparency, and independence, your time as Fed Chairman has been a failure...

source

Alan Greenspan refused to look for bubbles or try to do anything other than create them...

Under your watch, the Bernanke Put became a bailout for all large financial institutions...

But since then, you have decided that just about every large bank, investment bank, insurance company, and even some industrial companies are too big to fail. Rather than making management, shareholders, and debt holders feel the consequences of their risk-taking, you bailed them out. In short, you are the definition of moral hazard...

Even if all that were not true, the A.I.G. bailout alone is reason enough to send you back to Princeton...

From monetary policy to regulation, consumer protection, transparency, and independence, your time as Fed Chairman has been a failure...

source

Saturday, December 5, 2009

Skyscrapers and Economic Busts

Economist Andrew Lawrence came up with the Skyscraper’s Index. Apparently, the buildings go up in bubble economies. Then, the bubbles explode…leaving the buildings standing. The owners and builders typically go broke in the aftermath. Note the last line of the chart.

Economist Andrew Lawrence came up with the Skyscraper’s Index. Apparently, the buildings go up in bubble economies. Then, the bubbles explode…leaving the buildings standing. The owners and builders typically go broke in the aftermath. Note the last line of the chart.Generally, the skyscraper project is announced and construction is begun during the late phase of the boom in the business cycle; when the economy is growing and unemployment is low. This is then followed by a sharp downturn in financial markets, economic recession or depression, and

significant increases in unemployment. The skyscraper is then completed during the early phase of the economic correction, unless that correction was revealed early enough to delay or scrap plans for construction.

Friday, December 4, 2009

Unemployment Rate for November: 10.0%

The unemployment rate improved from the 26-year low reported in October and even the broader measure of "underemployment" - including discouraged workers and those settling for part-time work instead of full-time - was better, falling from last month's all-time high of 17.5 percent to 17.2 percent.

The unemployment rate improved from the 26-year low reported in October and even the broader measure of "underemployment" - including discouraged workers and those settling for part-time work instead of full-time - was better, falling from last month's all-time high of 17.5 percent to 17.2 percent.The average work week rose from a record low of 33.0 hours to 33.2 hours and average hourly earnings increased, all signs that employers are getting more out of current employees before hiring new ones.

Thursday, December 3, 2009

No Rubber Stamp for Bernanke Re-Nomination

Sen. Bernie Sanders, I-Vt., said late Wednesday that he will put a hold on Bernanke's nomination. A hold is an informal practice in which a senator informs the majority leader that he does not want a measure or nomination to reach the floor for a vote.

"The American people overwhelmingly voted last year for a change in our national priorities to put the interest of ordinary people ahead of the greed of Wall Street and the wealthy few," said Sanders, one of Bernanke's sharpest critics, in a statement. "What American people did not bargain for was another four years for one of the key architects of the Bush economy."

Sanders said Bernanke, who took the helm of the Fed in 2006, could have averted the financial crisis in several ways, but failed at "core responsibility of the Federal Reserve" and thus "it's time for him to go."

Among the litany of reasons he cited for his move, the statement from Sanders' office noted that unemployment had more than doubled under Bernanke's watch and more than 120 banks have failed since he became chairman.

read the CNN article

"The American people overwhelmingly voted last year for a change in our national priorities to put the interest of ordinary people ahead of the greed of Wall Street and the wealthy few," said Sanders, one of Bernanke's sharpest critics, in a statement. "What American people did not bargain for was another four years for one of the key architects of the Bush economy."

Sanders said Bernanke, who took the helm of the Fed in 2006, could have averted the financial crisis in several ways, but failed at "core responsibility of the Federal Reserve" and thus "it's time for him to go."

Among the litany of reasons he cited for his move, the statement from Sanders' office noted that unemployment had more than doubled under Bernanke's watch and more than 120 banks have failed since he became chairman.

read the CNN article

Wednesday, December 2, 2009

Tuesday, December 1, 2009

source

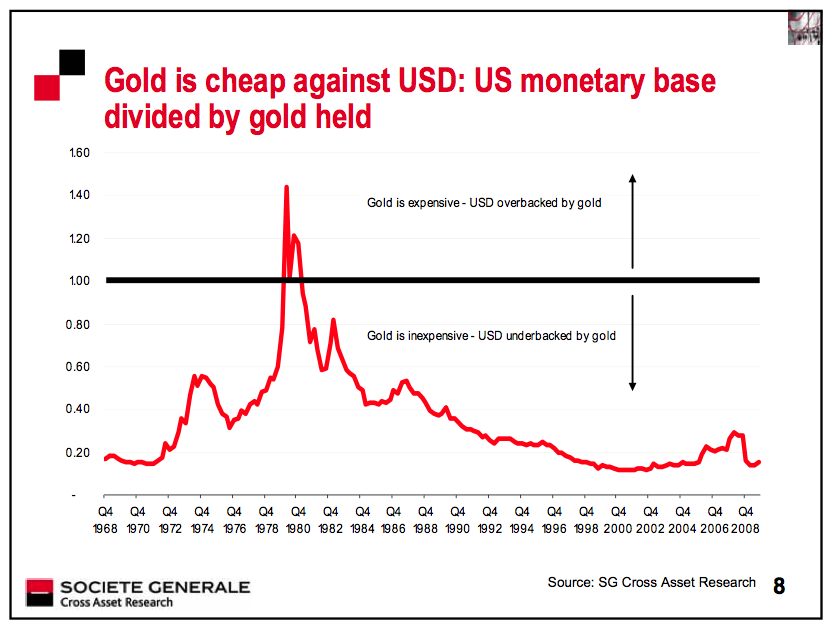

sourceGold is Cheap

source

My thoughts: Gold recently surpassed the $1200 mark. It reamains cheap. Marc Faber has predicted $5000 gold

Jacob Hornberger: Capitalism Has Not Failed

Suppose you were to give a one-question test in public schools across the country and, for that matter, to all graduates of U.S. public high schools: “True or False: The Great Depression was caused by the failure of America’s free-enterprise system.”

There can really be no doubt about what the answer would be. The vast majority of respondents would answer: True.

Yet, the correct answer is False. As Milton Friedman, Ludwig von Mises, Friedrich Hayek, Murray Rothbard, and others have documented so well, the Great Depression was caused by the Federal Reserve, America’s central bank, a federal institution that is antithetical to free enterprise...

Alas, the deception and delusion are not limited to the Great Depression.

Today, we might well be witnessing the death throes of America’s welfare state and warfare state. Everywhere you look, the entire statist system is in crisis or chaos.

Social Security, Medicare, Medicaid, Fannie Mae, Freddie Mac, FDIC, the drug war, Iraq, Afghanistan, the dollar, federal spending, the national debt, stimulus plans, foreign aid, nationalizations, corporate and banking bailouts, and on and on.

The whole welfare-warfare system is busted, broke, bankrupt. With each passing day, it gets worse and worse, as federal officials continue to double down their bets in the hopes that somehow the system is going to come out fine.

But notice what the statists are saying: That it’s not socialism or imperialism that have failed, it’s free enterprise!

read the entire essay

There can really be no doubt about what the answer would be. The vast majority of respondents would answer: True.

Yet, the correct answer is False. As Milton Friedman, Ludwig von Mises, Friedrich Hayek, Murray Rothbard, and others have documented so well, the Great Depression was caused by the Federal Reserve, America’s central bank, a federal institution that is antithetical to free enterprise...

Alas, the deception and delusion are not limited to the Great Depression.

Today, we might well be witnessing the death throes of America’s welfare state and warfare state. Everywhere you look, the entire statist system is in crisis or chaos.

Social Security, Medicare, Medicaid, Fannie Mae, Freddie Mac, FDIC, the drug war, Iraq, Afghanistan, the dollar, federal spending, the national debt, stimulus plans, foreign aid, nationalizations, corporate and banking bailouts, and on and on.

The whole welfare-warfare system is busted, broke, bankrupt. With each passing day, it gets worse and worse, as federal officials continue to double down their bets in the hopes that somehow the system is going to come out fine.

But notice what the statists are saying: That it’s not socialism or imperialism that have failed, it’s free enterprise!

read the entire essay

The Economic Crisis Continues

1. The US headline Consumer Price Index indicates deflation

2. A record nine million Americans, more than at any other time, are working part-time for economic reasons

3. U6, the “real” unemployment measure, has hit new highs… and, when you include workers who’ve given up on finding a job, unemployment rises to 21.1 percent

4. 33 percent of the unemployed have been looking for jobs for over six months, more than ever before

5. Available jobs continue to decrease at a much steeper rate than in an average recession… 18 million brand new jobs must be created over the next five years in order to return employment to 2007 levels

6. US consumer borrowing is grinding to a halt and personal saving has turned sharply higher

7. Prime mortgage delinquency rates are rising and are increasingly mirroring the subprime problem

8. The recovery is most likely to be a W-shaped… and we still have yet to hit even the first bottom

9. Bank lending to both consumers and businesses has fallen off dramatically

10. Money supply, as measured by M2, has stayed flat and the velocity of money is way down

11. Government tax receipts have tanked, and by almost

source and slideslow presentation

2. A record nine million Americans, more than at any other time, are working part-time for economic reasons

3. U6, the “real” unemployment measure, has hit new highs… and, when you include workers who’ve given up on finding a job, unemployment rises to 21.1 percent

4. 33 percent of the unemployed have been looking for jobs for over six months, more than ever before

5. Available jobs continue to decrease at a much steeper rate than in an average recession… 18 million brand new jobs must be created over the next five years in order to return employment to 2007 levels

6. US consumer borrowing is grinding to a halt and personal saving has turned sharply higher

7. Prime mortgage delinquency rates are rising and are increasingly mirroring the subprime problem

8. The recovery is most likely to be a W-shaped… and we still have yet to hit even the first bottom

9. Bank lending to both consumers and businesses has fallen off dramatically

10. Money supply, as measured by M2, has stayed flat and the velocity of money is way down

11. Government tax receipts have tanked, and by almost

source and slideslow presentation

{kind=link}

Subscribe to:

Posts (Atom)