Showing posts with label recession. Show all posts

Showing posts with label recession. Show all posts

Thursday, October 20, 2011

Tuesday, October 4, 2011

Friday, May 6, 2011

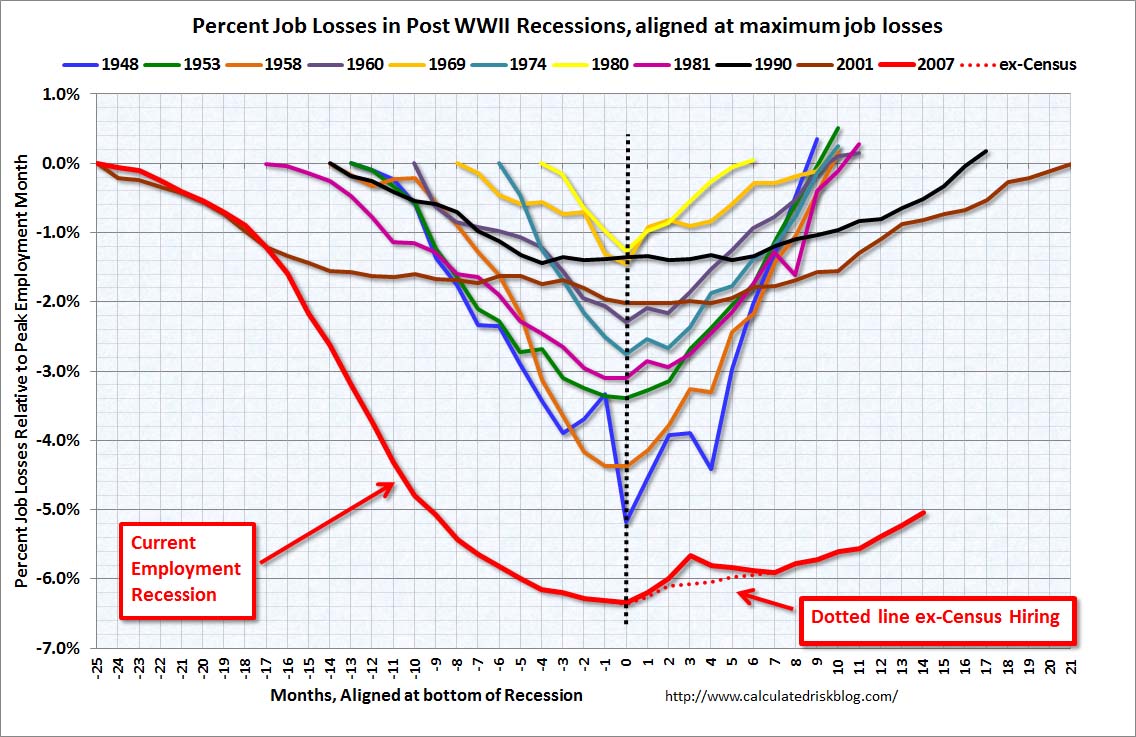

April Unemployment: 9%

The current employment recession is by far the worst recession since WWII in percentage terms, and 2nd worst in terms of the unemployment rate (only the early '80s recession with a peak of 10.8 percent was worse).

Monday, March 28, 2011

Job Loss by Recession

The employment graph shows the percentage of payroll jobs lost during post WWII recessions - aligned at maximum job losses.This shows the severe job losses during the recent recession - there are currently 7.5 million fewer jobs in the U.S. than when the recession started.

The employment graph shows the percentage of payroll jobs lost during post WWII recessions - aligned at maximum job losses.This shows the severe job losses during the recent recession - there are currently 7.5 million fewer jobs in the U.S. than when the recession started. Monday, March 7, 2011

Monday, January 31, 2011

Sunday, November 7, 2010

Saturday, October 30, 2010

Thursday, October 21, 2010

Cartoon: Inflation

As the Fed’s stated intention to execute QE2 lurks ever closer — plans to resume asset purchases, including Treasuries, are slated for the November 2nd FMOC meeting — even a few more than average regional Fed bank presidents are breaking rank.

According to Bloomberg, Philadelphia president Charles Plosser said unemployment is a “terrible problem,” but he flat out prefers it “to monetary-policy solutions at this point,” that increase inflation. Even more plainly, he said, “I am less inclined to want to follow a policy that is highly concentrated on raising inflation and raising inflation expectations.”

Nonetheless, QE2 will likely proceed as planned, and many already hard hit by recession will find their remaining dollars even less valuable.

Saturday, October 9, 2010

Friday, October 8, 2010

Rothbard on Depressions and their Cures

Thus, what the government should do, according to the Misesian analysis of the depression, is absolutely nothing. It should, from the point of view of economic health and ending the depression as quickly as possible, maintain a strict hands off, "laissez-faire" policy. Anything it does will delay and obstruct the adjustment process of the market; the less it does, the more rapidly will the market adjustment process do its work, and sound economic recovery ensue.

The Misesian prescription is thus the exact opposite of the Keynesian: It is for the government to keep absolute hands off the economy and to confine itself to stopping its own inflation and to cutting its own budget.

source

The Misesian prescription is thus the exact opposite of the Keynesian: It is for the government to keep absolute hands off the economy and to confine itself to stopping its own inflation and to cutting its own budget.

source

Monday, September 20, 2010

Saturday, September 11, 2010

How to" Fix" a Recession

What does Mises say should be done, say by government, once the depression arrives?

What is the governmental role in the cure of depression? In the first place, government must cease inflating as soon as possible. It is true that this will, inevitably, bring the inflationary boom abruptly to an end, and commence the inevitable recession or depression. But the longer the government waits for this, the worse the necessary readjustments will have to be. The sooner the depression-readjustment is gotten over with, the better. This means, also, that the government must never try to prop up unsound business situations; it must never bail out or lend money to business firms in trouble. Doing this will simply prolong the agony and convert a sharp and quick depression phase into a lingering and chronic disease.

The government must never try to prop up wage rates or prices of producers' goods; doing so will prolong and delay indefinitely the completion of the depression-adjustment process; it will cause indefinite and prolonged depression and mass unemployment in the vital capital goods industries.

The government must not try to inflate again, in order to get out of the depression. For even if this reinflation succeeds, it will only sow greater trouble later on.

The government must do nothing to encourage consumption, and it must not increase its own expenditures, for this will further increase the social consumption/investment ratio. In fact, cutting the government budget will improve the ratio.

What the economy needs is not more consumption spending but more saving, in order to validate some of the excessive investments of the boom. Thus, what the government should do, according to the Misesian analysis of the depression, is absolutely nothing. It should, from the point of view of economic health and ending the depression as quickly as possible, maintain a strict hands off, "laissez-faire" policy. Anything it does will delay and obstruct the adjustment process of the market; the less it does, the more rapidly will the market adjustment process do its work, and sound economic recovery ensue.

What is the governmental role in the cure of depression? In the first place, government must cease inflating as soon as possible. It is true that this will, inevitably, bring the inflationary boom abruptly to an end, and commence the inevitable recession or depression. But the longer the government waits for this, the worse the necessary readjustments will have to be. The sooner the depression-readjustment is gotten over with, the better. This means, also, that the government must never try to prop up unsound business situations; it must never bail out or lend money to business firms in trouble. Doing this will simply prolong the agony and convert a sharp and quick depression phase into a lingering and chronic disease.

The government must never try to prop up wage rates or prices of producers' goods; doing so will prolong and delay indefinitely the completion of the depression-adjustment process; it will cause indefinite and prolonged depression and mass unemployment in the vital capital goods industries.

The government must not try to inflate again, in order to get out of the depression. For even if this reinflation succeeds, it will only sow greater trouble later on.

The government must do nothing to encourage consumption, and it must not increase its own expenditures, for this will further increase the social consumption/investment ratio. In fact, cutting the government budget will improve the ratio.

What the economy needs is not more consumption spending but more saving, in order to validate some of the excessive investments of the boom. Thus, what the government should do, according to the Misesian analysis of the depression, is absolutely nothing. It should, from the point of view of economic health and ending the depression as quickly as possible, maintain a strict hands off, "laissez-faire" policy. Anything it does will delay and obstruct the adjustment process of the market; the less it does, the more rapidly will the market adjustment process do its work, and sound economic recovery ensue.

The Misesian prescription is thus the exact opposite of the Keynesian: It is for the government to keep absolute hands off the economy and to confine itself to stopping its own inflation and to cutting its own budget.

Monday, August 9, 2010

Four Bears

The August 6th S&P 500 close is the final data point for the Four Bad Bears chart. The timeline was established by the length of the 1929-1932 Dow crash, and today we reach the equivalent point following the S&P high of 2007.

source

Wednesday, July 28, 2010

Jim Rogers: New Recession in 2012

Speaking in an interview with business television channel CNBC, the septuagenarian investor said that "since the beginning of time" there has been a recession every four-to-six years, and that's mean another one is due around 2012.

However, he said that due to the extraordinary measures already adopted by central banks and governments around the world, the arsenal of available tools to combat the next recession is somewhat lacking.

With reference to Ben Bernanke, chairman of the US Federal Reserve, he said: "Is Mr Bernanke going to print more money than he already has? No, the world would run out of trees."

sourceFriday, July 9, 2010

Is a Depression All Bad?

Maybe a depression wouldn’t be so bad, after all.

The gist of the argument against depression is that people lose their jobs, incomes go down, companies go bankrupt and so forth. Is that all? Well, in general, people have less stuff…and less money to buy more stuff.

If that were all there was to it, it would seem like a small price to pay for the benefits of a depression. After all, a depression would wring the debt out of the economy. It would get rid of weak businesses. It would turn spendthrift households into savers. That’s got to be worth something.

The large presumption behind these worries is that, in a depression, people do not get what they want…they are disappointed. They are poor. They wear shoes with holes in them and drive old cars. They vote for Democrats and start reading Das Kapital.

Big deal.

What actually causes a depression, anyway? People choose to save rather than spend. Reduced demand causes a drop in sales…an increase in unemployment…falling prices and all the other nasty things we associate with a ‘depression.’ And yet, behind it is something people really want – savings. And behind the desire for savings are very real calculations and concerns. Without savings, people cannot retire comfortably. Without savings, they cannot withstand financial shocks and setbacks. Without savings, they may not be able to take advantage of opportunities that come their way.

In other words, there is a depression because people would rather have savings than a new car, or a new pair of shoes, or a vacation. In other words, people choose to have their cake rather than to eat it. What’s wrong with that?

Nothing. But it causes the economists’ GDP meters to tick over in a direction they don’t like…or at least in a direction they think they can do something about. The economists’ answer to this is to let the people have their savings…but to counteract the economic affect of higher savings rates with increased government spending.

It sounds so neat…so clean…so symmetrical. You might almost think it made sense, if you don’t think about it too much.

But wait. Where do the feds get any money to spend? They have to take up the savings. They take the cake! And there you have the problem right there. Resources have to come out of some other use – say, inventories, investments, whatever – and be put to use on government projects. We can safely assume that the federal projects are not the angel food, layered and frosted confections that the savers wanted to eat. Otherwise, they would have willingly paid for them themselves and there wouldn’t be a downturn in the first place. So, instead of savings and depression, the people get boondoggles and “growth.” Only it isn’t real growth. It is growth that flatters economists but leaves the rest of us hungry and disappointed. It is empty calories…measurable as “growth” on the economists’ GDP meters…but completely phony and not at all what people really wanted.

And what happened to their savings? They’ve been eaten up by the feds and their favored groups.

This whole Keynesian stimulus project is scammy from beginning to end. And in the middle too.

read the entire essay

The gist of the argument against depression is that people lose their jobs, incomes go down, companies go bankrupt and so forth. Is that all? Well, in general, people have less stuff…and less money to buy more stuff.

If that were all there was to it, it would seem like a small price to pay for the benefits of a depression. After all, a depression would wring the debt out of the economy. It would get rid of weak businesses. It would turn spendthrift households into savers. That’s got to be worth something.

The large presumption behind these worries is that, in a depression, people do not get what they want…they are disappointed. They are poor. They wear shoes with holes in them and drive old cars. They vote for Democrats and start reading Das Kapital.

Big deal.

What actually causes a depression, anyway? People choose to save rather than spend. Reduced demand causes a drop in sales…an increase in unemployment…falling prices and all the other nasty things we associate with a ‘depression.’ And yet, behind it is something people really want – savings. And behind the desire for savings are very real calculations and concerns. Without savings, people cannot retire comfortably. Without savings, they cannot withstand financial shocks and setbacks. Without savings, they may not be able to take advantage of opportunities that come their way.

In other words, there is a depression because people would rather have savings than a new car, or a new pair of shoes, or a vacation. In other words, people choose to have their cake rather than to eat it. What’s wrong with that?

Nothing. But it causes the economists’ GDP meters to tick over in a direction they don’t like…or at least in a direction they think they can do something about. The economists’ answer to this is to let the people have their savings…but to counteract the economic affect of higher savings rates with increased government spending.

It sounds so neat…so clean…so symmetrical. You might almost think it made sense, if you don’t think about it too much.

But wait. Where do the feds get any money to spend? They have to take up the savings. They take the cake! And there you have the problem right there. Resources have to come out of some other use – say, inventories, investments, whatever – and be put to use on government projects. We can safely assume that the federal projects are not the angel food, layered and frosted confections that the savers wanted to eat. Otherwise, they would have willingly paid for them themselves and there wouldn’t be a downturn in the first place. So, instead of savings and depression, the people get boondoggles and “growth.” Only it isn’t real growth. It is growth that flatters economists but leaves the rest of us hungry and disappointed. It is empty calories…measurable as “growth” on the economists’ GDP meters…but completely phony and not at all what people really wanted.

And what happened to their savings? They’ve been eaten up by the feds and their favored groups.

This whole Keynesian stimulus project is scammy from beginning to end. And in the middle too.

read the entire essay

Friday, May 28, 2010

1st Quarter 2010 GDP revised down to 3.0%

There are really two measures of GDP: 1) real GDP, and 2) real Gross Domestic Income (GDI). The BEA also released GDI today. Recent research suggests that GDI is often more accurate than GDP...

There are really two measures of GDP: 1) real GDP, and 2) real Gross Domestic Income (GDI). The BEA also released GDI today. Recent research suggests that GDI is often more accurate than GDP...The following graph is constructed as a percent of the previous peak in both GDP and GDI. This shows when the indicator has bottomed - and when the indicator has returned to the level of the previous peak. If the indicator is at a new peak, the value is 100%. The recent recession is marked as ending in Q3 2009 - this is preliminary and NOT an NBER determination...

It appears that GDP bottomed in Q2 2009 and GDI in Q3 2009. Real GDP is only 1.2% below the pre-recession peak - but real GDI is still 2.3% below the previous peak.

GDI suggests the recovery has been more sluggish than the headline GDP report and better explains the weakness in the labor market.

source

Tuesday, April 27, 2010

Thursday, April 15, 2010

Common Fallacies about Macroeconomics

As the recession has deepened and the financial debacle has passed from one flare-up to another during the past year and a half, commentary on the economy’s troubles has swelled tremendously...

The bulk of it has been bad for the same reasons. Most of the people who purport to possess expertise about the economy rely on a common set of presuppositions and modes of thinking. I call this pseudointellectual mishmash “vulgar Keynesianism.” It’s the same claptrap that has passed for economic wisdom in this country for more than fifty years and seems to have originated in the first edition of Paul Samuelson’s Economics...

Vulgar Keynesians are nothing if not policy activists...The eras they esteem as the most glorious ones in U.S. politicoeconomic history are Roosevelt’s first term as president and Lyndon B. Johnson’s first few years in the presidency. In these periods, we witnessed an outpouring of new government measures to spend, tax, regulate, subsidize, and generally create economic mischief on an extraordinary scale. The Obama administration’s ambitious plans for government action on many fronts fill vulgar Keynesians with hope that a third such Great Leap Forward has now begun.

The vulgar Keynesian does not understand that extreme policy activism may work against economic prosperity by creating what I call “regime uncertainty,” a pervasive uncertainty about the very nature of the impending economic order, especially about how the government will treat private-property rights in the future.

source

The bulk of it has been bad for the same reasons. Most of the people who purport to possess expertise about the economy rely on a common set of presuppositions and modes of thinking. I call this pseudointellectual mishmash “vulgar Keynesianism.” It’s the same claptrap that has passed for economic wisdom in this country for more than fifty years and seems to have originated in the first edition of Paul Samuelson’s Economics...

Vulgar Keynesians are nothing if not policy activists...The eras they esteem as the most glorious ones in U.S. politicoeconomic history are Roosevelt’s first term as president and Lyndon B. Johnson’s first few years in the presidency. In these periods, we witnessed an outpouring of new government measures to spend, tax, regulate, subsidize, and generally create economic mischief on an extraordinary scale. The Obama administration’s ambitious plans for government action on many fronts fill vulgar Keynesians with hope that a third such Great Leap Forward has now begun.

The vulgar Keynesian does not understand that extreme policy activism may work against economic prosperity by creating what I call “regime uncertainty,” a pervasive uncertainty about the very nature of the impending economic order, especially about how the government will treat private-property rights in the future.

source

Friday, April 2, 2010

March Unemployment: 9.7%

The economy has lost 2.3 million jobs over the last year, and 8.2 million jobs since the beginning of the current employment recession.

The unemployment rate was steady at 9.7 percent.

For the current recession, employment peaked in December 2007, and this recession is by far the worst recession since WWII in percentage terms, and 2nd worst in terms of the unemployment rate (only early '80s recession with a peak of 10.8 percent was worse).

source

Subscribe to:

Posts (Atom)